{kind=link}

![]()

Apple CEO Tim Cook dinner (left) with CFO Luca Maestri

AppleInsider might earn an affiliate fee on purchases made by way of hyperlinks on our web site.

Apple will likely be asserting its 2023 fiscal first quarter outcomes on February 2. Here is what to anticipate from the vacation quarter earnings — and what Wall Road is predicting.

Apple revealed on January 4 that it will likely be holding its investor call on Thursday, February 2, at 2:00 PM Pacific, 5:00 PM Japanese, to debate the primary fiscal quarter earnings launch from earlier within the day. Primarily based on the standard timeline for outcomes, particulars ought to be launched by Apple about half an hour earlier than the decision itself.

For the decision, CEO Tim Cook and Luca Maestri will talk about the well being of Apple during the last three months, together with product launches and gross sales, detrimental occasions, and different financial headwinds that would have an effect on the quarters to come back.

As typical for Apple for the reason that begin of the pandemic, the corporate hasn’t supplied formal income steering for the quarter on the time of its earlier earnings report.

Earnings for the quarter are usually the very best as a consequence of Apple’s extremely seasonal gross sales, in addition to an inventory of key product launches.

Nonetheless, unusually for the quarter, Apple did situation an uncharacteristic notice about iPhone manufacturing in November. Attributable to COVID-19 points at Foxconn’s Zhengzhou factory, the availability of the iPhone 14 Pro and iPhone 14 Professional Max was interrupted, prompting Apple’s discover.

On the time, the press launch admitted the manufacturing unit operated at a “considerably diminished capability,” although it has since caught up. Apple additionally mentioned it continued to see “robust demand” for the Professional fashions, but additionally anticipated decrease shipments and longer wait instances for purchasers.

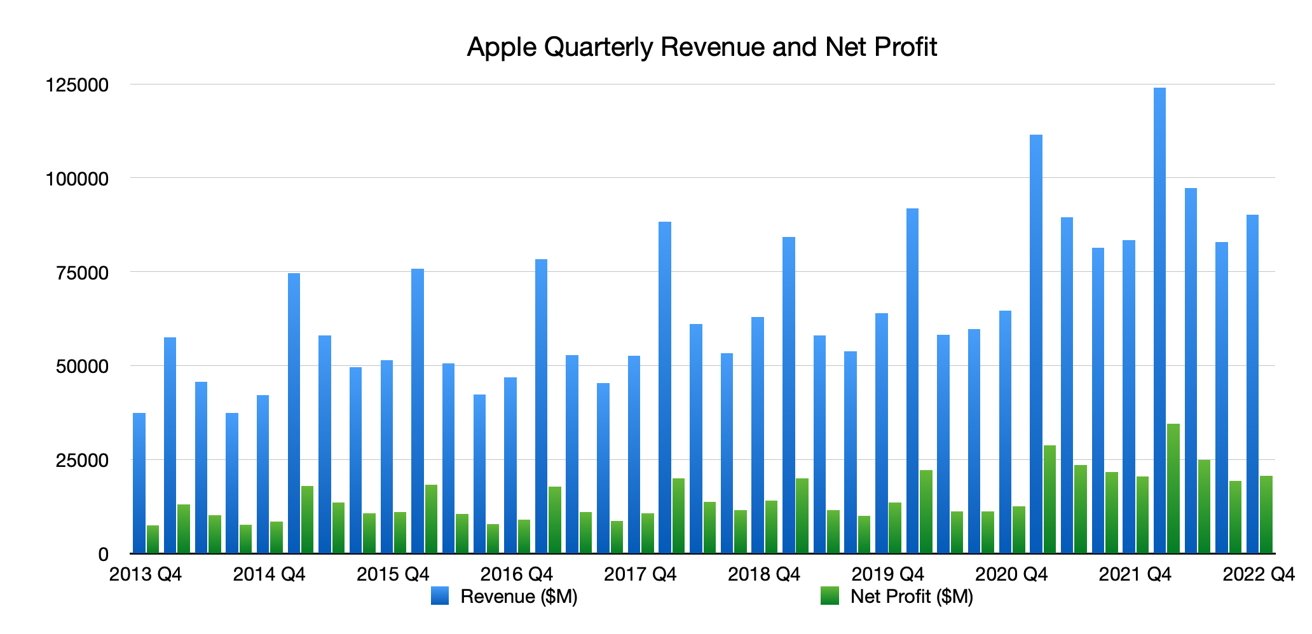

Apple’s Q1 2023 figures must beat significantly excessive figures reported one yr in the past in Q1 2022. At the moment, it reported an 11.2% YoY enhance in income to $123.9 billion, with a internet revenue of $34.6 billion additionally record-setting and an annual enhance of 20.4%.

For Q1 2022, the iPhone introduced in $71.6 billion in income, with Mac income additionally as much as $10.8 billion within the quarter. Wearables, Dwelling, and Equipment was as much as $14.7 billion in income, Providers noticed a YoY enhance to $19.5 billion, however iPad income noticed a drop right down to $7.2 billion.

What’s the Wall Road consensus on Apple’s vacation quarter?

As of January 23, the analyst consensus for the quarter is an earnings per share of $1.95. This interprets into 1 / 4 with $122 billion in income. This compares to $123.9 billion within the year-ago quarter.

Consensus for the subsequent quarter’s income is presently sitting at $98.2 billion, however many of the analysts in query chimed in earlier than the discharge of the brand new Mac Professional, up to date Mac minis, and a second-generation massive HomePod.

Particular person analysts on Apple

The iPhone 14 Professional cargo issues had been some extent of situation for analysts analyzing the corporate’s fortunes, with lower shipment forecasts of the fashions thought to closely affect income. Nonetheless, some supplied the view that shipments can be pushed into Q2 2023 gross sales as a substitute.

Apple’s quarterly income and internet revenue as of This autumn 2022

At one level in January, Apple’s market capitalization dipped below $2 trillion, with buyers cautious of the availability chain issues and listening to analyst discussions on the corporate’s fortunes.

Daniel Ives and John Katsingris, Wedbush

Wedbush lowered its worth goal for Apple from $200 to $175 on January 4, on the premise of it being a extra “unsure setting” for buying and selling, and over demand headwinds.

“Apple stays our favourite tech identify,” the agency mentioned whereas insisting it maintains its “Outperform” score for the inventory, however provide chain checks had been “clearly combined heading into the subsequent few quarters,” with Apple additionally apparently chopping again some orders for merchandise.

On iPhone, demand for the iPhone 14 Professional is extra steady than feared, and that there’s a perception that the “total demand setting is extra resilient than the Road is anticipating.”

Samik Chatterjee, JP Morgan

On January 19, JP Morgan warned buyers it believes demand is falling barely throughout the whole Apple product catalog. Viewing the earnings as a “robust setup” as a consequence of provide headwinds, the concerns changed into “demand issues for the Mar-Q and past,” the agency believes.

Income and earnings for the primary quarter of 2023 will “monitor modestly beneath consensus expectations,” however the miss ought to be “extra modest” than beforehand anticipated. JP Morgan additionally raised its December quarter estimates on provide monitoring, however added that weak spot in underlying demand will make the subsequent quarter “equally robust.”

After reducing the value goal in December 2022 from $200 to $190, JP Morgan went additional in January, pushing it to $180.

Canaccord

A January 22 be aware had Canaccord Genuity Capital Markets reduce its worth goal for Apple from $200 to $170, whereas reaffirming the “purchase” score for inventory.

Demand for the Professional mannequin iPhones has been disappointing, however believes some misplaced December gross sales will likely be pushed later into March. Current channel checks point out {that a} four-week look ahead to the premium fashions has all however evaporated.

Total demand has been slowing regardless of a powerful sell-through for iPhones, it provides, which presents a extra pessimistic view for 2023 as a complete. There is a forecast of $68.3 billion for first-quarter iPhone gross sales, with a full-year estimate of $199.6 billion.

Different {hardware} can also be prone to a significant decline in demand, with the upper worth factors of recent Macs making it exhausting for Canaccord to see if shoppers nonetheless have a “willingness to put money into costlier merchandise” given a tricky macro backdrop.

Rosenblatt

On January 13, Rosenblatt Securities reduced its worth goal by $24 right down to $165, with iPhone manufacturing delays and “macro companies headwinds” in charge.

A December survey discovered fewer folks prepared to purchase or have purchased an iPhone 14 than an identical survey in September, with shopping for intent for the iPhone 14 Professional Max lowering from 44% in September to 34% in December for that group.

Rosenblatt additionally echoed reviews that the App Retailer has slowed down, together with a double-digit % drop within the December quarter following progress earlier within the yr, which is “doubtlessly reflecting weakening sport revenues.”

Finally, the analysts count on enhancements and affords that buyers might view this “as a throwaway quarter” and to as a substitute “deal with later durations.”

AppleInsider will likely be including extra analyst predictions earlier than the earnings report.

Source link