{kind=link}

Editor’s take: Undeniably, we normally spend a number of time speaking about forefront semiconductor manufacturing. It is a frequent mistake that everybody falls into when discussing semis, one which we’re as responsible of as anybody. The world is rightly centered on the shortage of firms able to working at the vanguard, however there may be much more to semis.

Editor’s Observe:

Visitor creator Jonathan Goldberg is the founding father of D2D Advisory, a multi-functional consulting agency. Jonathan has developed progress methods and alliances for firms within the cellular, networking, gaming, and software program industries.

We just lately went looking for information on fab capability by course of nodes, and everybody agreed that the main knowledgeable on the topic is Bill McClane at IC Insights. He maintains one of the rigorous fashions on the market on the topic, and rightly costs a premium for his experiences. That is must-read materials for anybody planning out a multi-year semis roadmap.

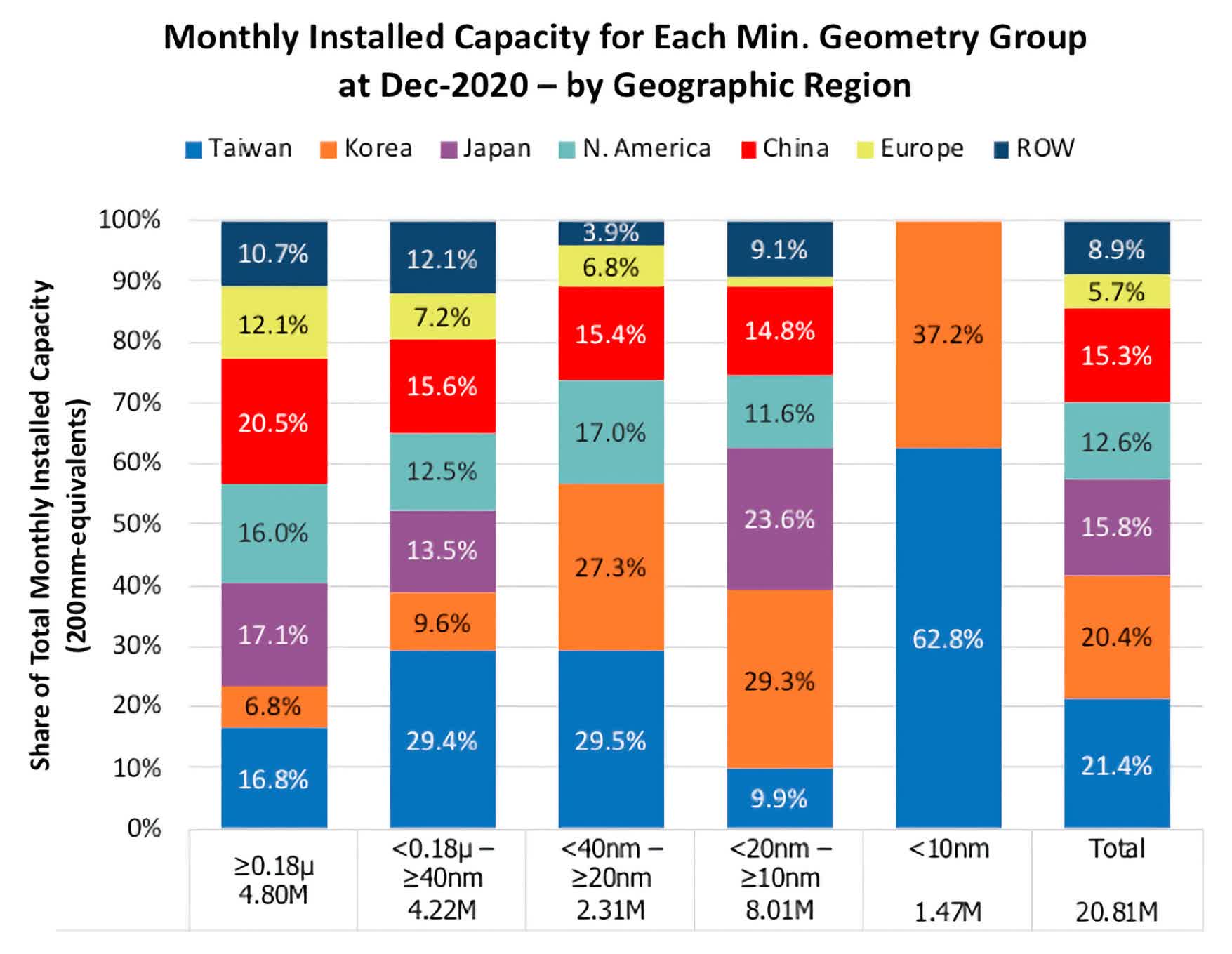

A fast Google search yielded this excerpt from IC Perception’s information, and it tells an essential story…

Over 90% of the world’s semiconductor capability is working at 10nm or above. We are able to argue about the place to attract the dividing line, however it’s secure to say that the overwhelming majority of capability operates on the trailing edge.

That is essential for numerous causes.

First, when the world ran out of semiconductors in 2020/2021 – most of these shortages have been occurring in these extra mature processes. TSMC’s main clients have been all in a position to get a lot of the capability they wanted at 7nm, however there was actual ache for industrial and automotive clients.

These firms wanted prosaic elements like microcontrollers (MCUs) and energy administration ICs (PMICs), and these merchandise are typically produced at older nodes. Right now, at the same time as the provision shortages have turned to extra stock in lots of classes, the older merchandise are simply catching up with the pent up demand from two years in the past.

Secondly, the US authorities is at the moment struggling to resolve find out how to allocate $52 billion of CHIPS Act funds. If the purpose of these funds is merely to convey forefront processes again to the US, then go forward and provides all the cash to Intel. They are going to dividend out $7 billion or $8 billion to shareholders and proceed with their plan to compensate for manufacturing that they must implement anyway.

Then again, if the aim is to actually safe the US semis provide chain, then maybe a greater plan is to divide that cash up extra broadly. Ideally, they’d spend the cash to plant a number of seeds resulting in new firm formation and in primary tutorial analysis, which may then be commercialized by the personal sector. Sadly, there are not any straightforward mechanisms for doing this but, and so one other strategy is to divide up the funds amongst a broad swathe of US firms concerned in semis manufacture, as long as they decide to will increase in US capability. This doesn’t simply imply fabs and foundries, but in addition wants to incorporate the instruments firms, robotics suppliers and chemical makers – the entire provide chain. Intel ought to get some, however not the vast majority of these funds.

In accordance with the Semiconductor Trade Affiliation, the CHIPS Act has had a constructive collateral effect by triggering the personal sector into investing some $200 billion for US semiconductor manufacturing.

Lastly, these numbers ought to remind us that the story is broader than simply TSMC and Samsung. There may be nonetheless a number of attention-grabbing, essential work being completed on the trailing edge foundries.

The obvious instance of that is International Foundries. GloFo shouldn’t be on the lead in silicon manufacture however it has carved up some very sizable “niches” like silicon on insulator (SOI) and Silicon Carbide. And whereas they don’t have the close to duopoly on this that TSMC and Samsung get pleasure from with 7nm, they arrive shut with a lot of their SOI strains. If for any motive the US ever misplaced entry to TSMC, GloFo would arguably be as essential part of the answer as Intel.

Source link