{kind=link}

The numbers hardly ever add up. That’s the drawback IAB Europe got down to deal with on March 12, 2026, when it revealed the third paper in its five-part sequence on the convergence of commerce and media in retail media – this time with a topic that almost all trade conversations quietly sidestep: accounting.

Produced in collaboration with Mediasense and authored by Lauren Wakefield, the paper is titled “The Convergence and Coexistence of Commerce and Media in Retail Media Collection – Half 3: Retailer Accounting for Retail Media Gross sales.” It targets a basic structural drawback. In response to the doc, even amongst publicly listed corporations, “commerce media” hardly ever seems as a clear, standalone line merchandise in monetary reporting, and when it does, the numbers could not align with the figures communicated by Commerce Media Community (CMN) management.

That disconnect shouldn’t be unintended. It’s, based on IAB Europe and Mediasense, largely a product of how accounting requirements deal with retail media gross sales within the first place.

The provider receipts drawback

On the coronary heart of the problem is a classification query. In response to the paper, gross sales of digital retail media by retailers are categorised in accounting phrases as provider receipts. The logic follows instantly from the industrial relationship: the advertiser that ordinarily provides items to the retailer is now additionally making funds to purchase media from that very same retailer. In accounting phrases, the 2 actions are intertwined.

Underneath Worldwide Monetary Reporting Requirements (IFRS), which govern reporting for almost all of publicly listed European corporations, provider receipts are presumed to be a discount within the buy value of products acquired from the advertiser. They’re netted towards the value of products offered (COGS) line merchandise, not recorded as incremental income. Comparable guidelines apply below US GAAP, with the related equivalents being ASC 606, ASC 280, and ASC 205-20.

The sensible consequence is important. As retail media grows, a retailer working below the default IFRS remedy would document lowering prices of products offered slightly than growing revenues. The highest line stays flat, or grows solely from product gross sales, whereas the good thing about retail media quietly offsets procurement prices beneath the gross revenue line.

Because of this sizing the retail media market remains so difficult. Analysts monitoring publicly reported income figures could also be taking a look at numbers that exclude a considerable and rising portion of what CMN management considers media earnings.

Three causes retailers need an alternate remedy

The paper identifies three incentives driving retailers to pursue an alternate accounting remedy – one which information retail media gross sales as revenues slightly than value offsets.

First, income is a key monetary metric. Rising it attracts constructive consideration internally from senior administration and externally from buyers and analysts. Second, retailers more and more view themselves as builders of media companies, not merely as corporations lowering the acquisition value of products. Recording retail media as income, based on the doc, extra precisely displays the underlying economics from their perspective. Third, there’s a funds entry dimension: if retail media spend is handled as advertising working expense on the advertiser aspect (slightly than an offset towards the advertiser’s personal revenues), it turns into simpler for digital retail media to attract from advertiser model advertising budgets – a bigger and usually extra versatile pool of funds than commerce budgets.

These pressures usually are not trivial. European retail media advertising reached €13.7 billion in 2024, a 21.1% improve year-over-year based on IAB Europe knowledge from October 2025. At that scale, whether or not income is classed above or beneath the gross revenue line has materials implications for the way buyers learn stability sheets.

For retailers to shift to income recognition slightly than COGS offset, the paper units out a rigorous commonplace. The retailer should display real independence – that the advertiser shopping for retail media was doing so individually from its standing because the retailer’s provider. In response to the doc, three circumstances govern when retail media might be counted as income.

The primary situation issues the contract construction. If gross sales of retail media are coated in the primary industrial provider settlement, the media will probably be deemed linked and offset towards the worth of products bought from that advertiser. Preserving retail media in a separate contract is a obligatory however not enough situation for income remedy.

The second situation is extra demanding. Even in a separate contract, the promoting have to be generic – brand-building or common value promotions – slightly than particular to the retailer. The paper supplies a pointy illustrative instance: if a retailer supplied top-pick banner placements or unique pricing, the profit shouldn’t be thought of distinct as a result of it capabilities as an incentive throughout the current industrial relationship. The advert gross sales would, in that case, stay as a value deduction to COGS no matter how the contract is structured.

The third situation requires the retailer to display that the retail media was offered at honest worth. That is an goal pricing check, and its implications stretch into how retailers set charge playing cards and negotiate placements with supplier-advertisers.

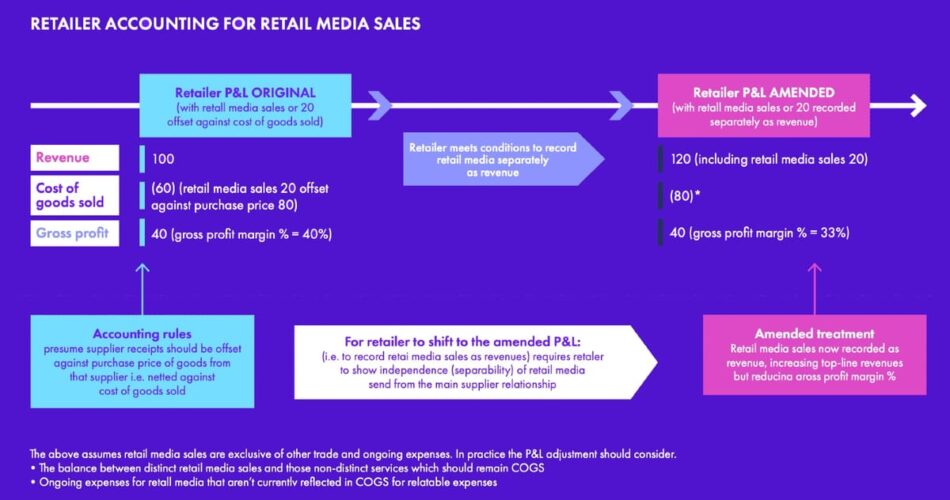

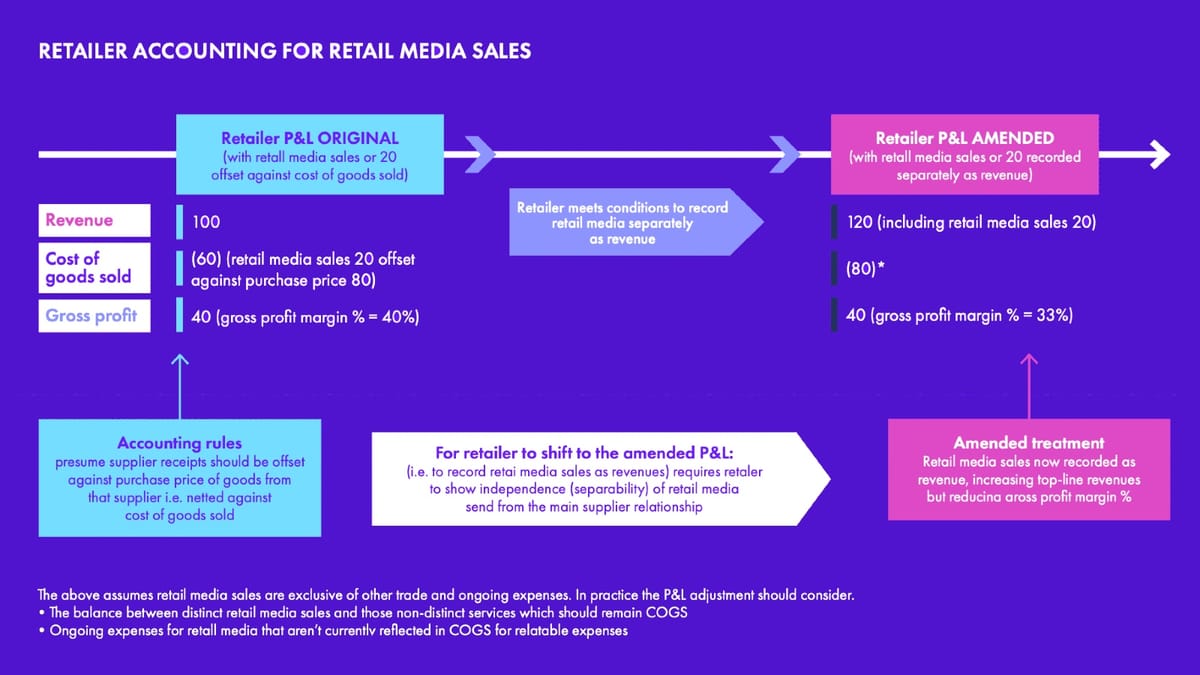

What this implies for the P&L

The paper features a labored instance that clarifies the stakes. Within the authentic P&L, a retailer information income of 100, value of products offered of 60 (with retail media gross sales of 20 already offset towards a purchase order value of 80), and gross revenue of 40 – a gross revenue margin of 40%.

Underneath the amended remedy, the place retail media gross sales of 20 are recorded individually as income, the highest line turns into 120. The price of items offered adjusts to 80. Gross revenue stays at 40, however the gross revenue margin share falls to 33%.

The headline income determine will increase, however the margin share declines. It is a level that deserves consideration. A retailer that efficiently reclassifies retail media as income will report a bigger prime line – but additionally a decrease gross margin. Analysts and buyers who monitor margin ratios slightly than absolute income figures could interpret the change otherwise relying on how effectively it’s defined in disclosure notes.

Market fashions: a distinct algorithm

The paper attracts a transparent distinction between conventional retailers and on-line marketplaces – a distinction with direct relevance for platforms corresponding to Amazon and eBay.

The important thing variable is the principal/agent query: does {the marketplace} take management of the products being offered? In response to the doc, if the net market buys the products, shops them in its warehouse, units the worth, and so forth, it’s performing as principal. In that situation, gross sales of retail media to suppliers will probably be offset towards the price of items bought from them, until the separability circumstances described above are glad.

If, nonetheless, the provider shops the stock, units the worth, and bears the returns danger, the net market is performing as agent. On this situation, there is no such thing as a value of products offered for {the marketplace} – it by no means owns the products. Any gross sales of digital retail media should subsequently robotically be recorded as income. The accounting remedy, on this case, shouldn’t be a alternative: it’s a structural final result of the enterprise mannequin.

This distinction helps clarify why sure market operators have persistently reported clear, rising retail media income traces whereas conventional grocery store retailers have confronted extra ambiguity in tips on how to current equal earnings.

Disclosure necessities below IFRS and US GAAP

No matter which remedy a retailer applies, disclosure obligations apply. In response to the paper, each IFRS and US GAAP require retailers and on-line marketplaces to reveal materials classes of earnings and their affect on income and/or value of products offered.

The related IFRS requirements are IFRS 15 (Income Recognition), IFRS 8 (Working Segments), and IAS 1 (Presentation of Monetary Statements). The US GAAP equivalents are ASC 606, ASC 280, and ASC 205-20. The paper summarizes the disclosure rule clearly: if retail media is reported individually throughout the data commonly reviewed by senior administration, it additionally deserves separate disclosure within the exterior annual report.

This is a vital level for the advertising group. If a retailer’s management staff receives common stories on retail media efficiency as a standalone enterprise phase, then buyers and analysts ought to, in precept, be capable to entry equal data within the annual report. The place that separate disclosure is absent, questions come up about whether or not retail media has been formally constituted as a definite inner reporting phase.

Generic promoting and the IFRS 15 check

The paper closes with a particular explainer on what makes promoting “generic” and subsequently eligible for distinct income recognition below IFRS 15. The usual it describes is demanding.

In response to the doc, promoting is barely distinct if it supplies a generic, retailer-agnostic profit – corresponding to model constructing or common promotions – slightly than help that’s particular to promoting via a specific retailer. The check is basically considered one of independence: does the promoting create worth that exists past the precise industrial relationship?

The paper affords a concrete illustration of promoting that passes the check: promotion of a provider’s model via non-price-specific messaging, delivered each on and off the retailer’s platform, directing customers to the provider’s personal web site slightly than to a retailer-exclusive product web page. This creates what the doc describes as broader demand era that exists independently of the buying and selling relationship. Such promoting meets the factors for being generic and distinct below IFRS 15 and might be acknowledged as income for the retailer.

This framing has direct implications for the way Commerce Media Networks construction their promoting merchandise. Networks that provide solely retailer-specific placements – as an illustration, sponsored positions tied completely to that retailer’s class hierarchy – could face a more durable case for income recognition than these providing broader brand-building codecs that run throughout channels.

The accounting questions raised on this paper have penalties effectively past the finance division. IAB Europe research has consistently found that 53% of buyers cite lack of standardization as the key barrier to retail media investment. The accounting inconsistencies described listed here are one structural purpose why commonplace comparisons are so troublesome to make.

If one retailer information retail media as income and one other nets it towards COGS, their reported monetary profiles look materially totally different – even when the underlying industrial preparations are equivalent. Market sizing workouts that combination publicly reported figures with out adjusting for this distinction will produce unreliable totals. That drawback has been famous at PPC Land in coverage of the IAB Europe retail media statistics and in evaluation of how commerce media maturity lags across industries.

Manufacturers and companies negotiating retail media offers may discover these distinctions commercially related. If a retailer buildings media gross sales inside the primary provider settlement, the accounting remedy on either side adjustments. Advertisers could discover that spend which they categorize as a advertising working expense is being handled by the retailer as a discount in buy value – with totally different tax and margin implications for every celebration.

IAB Europe has been pushing toward standardized definitions and measurement frameworks since not less than March 2025, when up to date pan-European definitions protecting on-site, off-site, and in-store retail media had been revealed. The certification programme, which noticed Albert Heijn become the first certified retail media network in September 2025, addresses measurement transparency. However accounting remedy sits upstream of measurement: it determines what figures enter the reporting pipeline within the first place.

The paper is the third in a five-part sequence. The primary two papers, “Defining Commerce and Media” (co-published with IAB US) and “The Case for Breaking Down Silos,” examined the problem via a enterprise and operational lens. IAB Europe has indicated that additional content material within the sequence will probably be launched within the coming weeks. The total paper is obtainable for obtain from the IAB Europe web site at 58.79 KB.

Timeline

- September 2024 – IAB and IAB Europe release the first industry-wide in-store retail media measurement standards for public comment

- January 25, 2025 – IAB Tech Lab finalizes OpenRTB specification updates for product itemizing advertisements to standardize programmatic commerce media transactions

- March 26, 2025 – IAB Europe publishes updated pan-European definitions for retail and commerce media

- July 15, 2025 – IAB Europe releases updated 101 Guide to Retail & Commerce Media 2025 Review and second annual Attitudes to Retail Media Report

- July 15, 2025 – European retail media partnerships extend, with brands working with 4-6 networks doubling to 24%

- September 4, 2025 – Omdia projects retail media to capture 20% of global advertising revenue by 2030, exceeding $300 billion

- September 9, 2025 – IAB and IAB Europe publish incrementality framework for commerce media budgets

- September 24, 2025 – Albert Heijn becomes first retail media network certified under IAB Europe programme

- October 7, 2025 – IAB Europe releases retail media statistics showing European retail media at €13.7 billion with 21.1% growth in 2024

- October 9, 2025 – IAB Europe opens public comment on updated Commerce Media Measurement Standards V2

- October 14, 2025 – IAB Europe releases updated Pan-European Retail & Commerce Media Landscape Map

- November 3, 2025 – IAB and IAB Europe release guidelines for incremental measurement in commerce media

- November 23, 2025 – Commerce media maturity lags across industries despite $1.3 trillion growth projection

- December 4, 2025 – IAB Ireland releases first dedicated retail media report for Irish market

- February 25, 2026 – IAB Finland publishes first comprehensive retail media landscape for Finnish market

- March 12, 2026 – IAB Europe and Mediasense publish Half 3 of the Convergence and Coexistence of Commerce and Media in Retail Media sequence, addressing retailer accounting remedy for retail media gross sales

Abstract

Who: IAB Europe and Mediasense, with the paper authored by Lauren Wakefield of IAB Europe.

What: The third paper in a five-part sequence inspecting the intersection of commerce and media in retail media, targeted particularly on how retailers and on-line marketplaces account for retail media gross sales below IFRS and US GAAP. The paper explains when retail media earnings might be recorded as income versus when it have to be netted towards value of products offered, and what circumstances govern every remedy.

When: Revealed on March 12, 2026, as a part of an ongoing sequence with additional papers anticipated within the coming weeks.

The place: Revealed by IAB Europe, the Brussels-based European-level affiliation for the digital advertising and promoting ecosystem, at iabeurope.eu.

Why: Accounting remedy instantly shapes how totally different Commerce Media Networks report, classify, and interpret their income – creating inconsistencies that complicate market sizing, investor comparisons, and funds choices by manufacturers and companies. As European retail media spending reached €13.7 billion in 2024 and continues to develop, the shortage of readability on how that income is acknowledged throughout corporations has change into a structural problem for the trade.

Share this text