{kind=link}

Chinese language on-line marketplaces are now not simply occasional cut price stops in English-speaking markets. Throughout the USA, UK, Canada, and Australia, platforms comparable to Temu, Shein, AliExpress, and TikTok Store have gotten a part of common procuring routines, with Omnisend’s newest survey displaying widespread annual utilization and rising repeat engagement throughout all 4 nations.

To know how these habits are altering, Omnisend surveyed 4,000 customers throughout the 4 markets.

This report additionally compares the most recent findings with Omnisend’s earlier market analysis from 2024 and 2025, enabling monitoring of how adoption, procuring frequency, and shopper sentiment have shifted over time.

Key findings

- Chinese language market adoption remained excessive throughout all 4 markets, reaching 71% within the USA, 75% within the UK, 73% in Canada, and 80% in Australia.

- Temu recorded the strongest utilization progress throughout the markets tracked since 2024.

- Within the USA, 46% of customers assist tariffs on imported items.

- Within the USA, 59% of customers say they’re keen to pay extra for merchandise labeled “Made within the USA.”

- Amongst buyers who diminished or stopped shopping for from Chinese language ecommerce platforms, the most typical causes have been worth will increase, product high quality considerations, unreliable delivery, and supply charges.

Chinese language market adoption charges 2024–2026: Temu, Shein, AliExpress, and TikTok Store

Chinese language ecommerce platforms are rising in all 4 markets examined in Omnisend’s survey. This development goes past simply occasional cut price looking. Over the previous 12 months, 71% of buyers within the USA, 75% within the UK, 73% in Canada, and 80% in Australia reported shopping for from at the very least one Chinese language market, comparable to Temu, Shein, AliExpress, or TikTok Store.

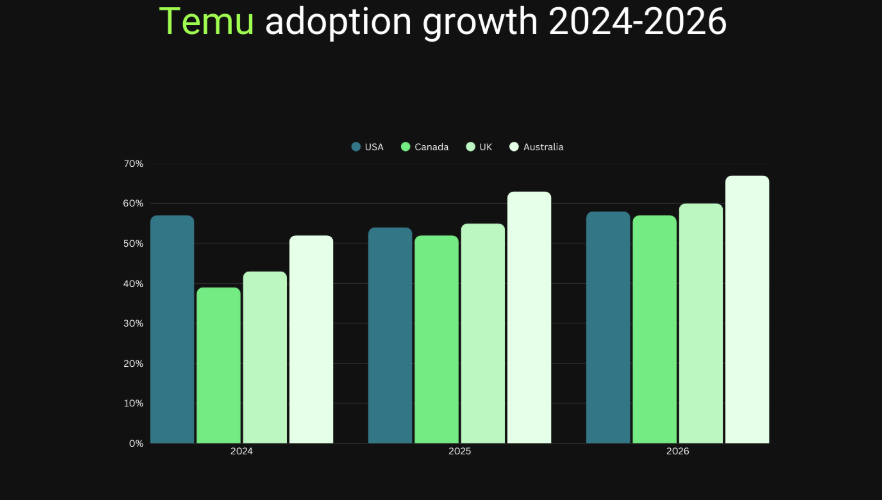

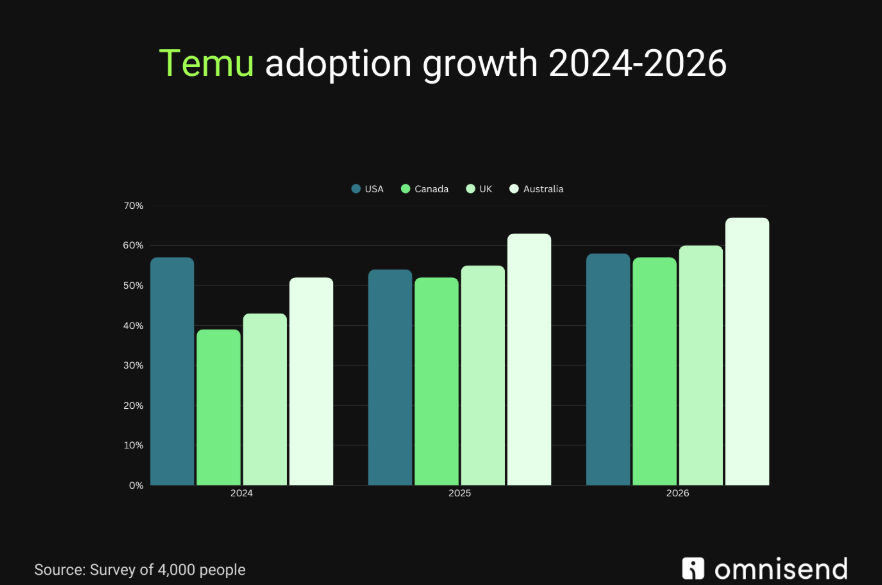

Temu exhibits the clearest long-term progress story. In contrast with 2024, its adoption rose from 57% to 58% within the USA, from 43% to 60% within the UK, from 39% to 57% in Canada, and from 52% to 67% in Australia.

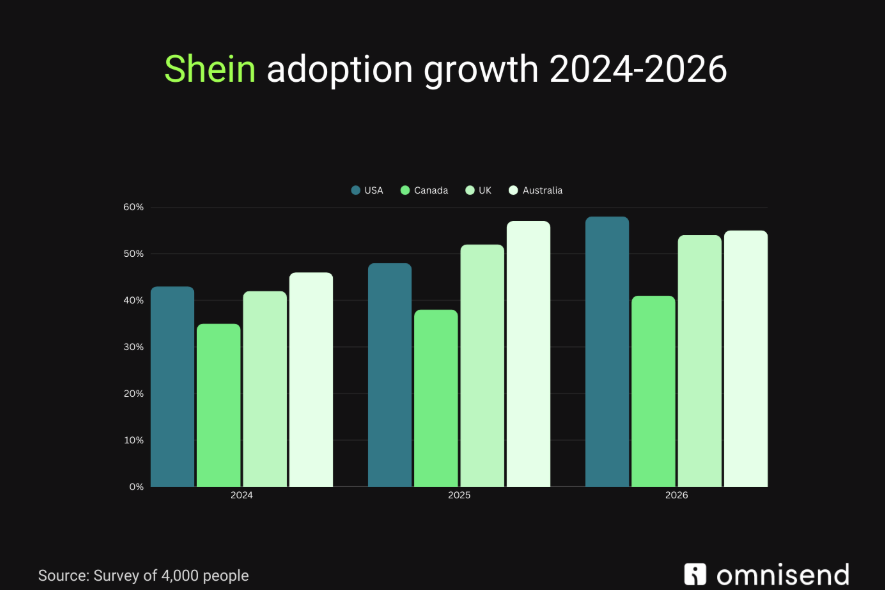

Shein additionally posted robust beneficial properties, climbing from 43% to 49% within the USA, from 42% to 54% within the UK, from 35% to 41% in Canada, and from 46% to 55% in Australia.

AliExpress noticed particularly notable progress within the UK and Australia. On the identical time, TikTok Store made a few of its greatest beneficial properties within the UK and the USA, suggesting the broader market ecosystem is strengthening somewhat than counting on a single platform. You will need to point out that Australia and Canada haven’t launched their respective native native TikTok Store vendor platforms.

The larger sign, although, is frequency. Month-to-month Temu procuring elevated throughout each market, rising from 22% to 36% within the USA, from 19% to 32% within the UK, from 21% to 29% in Canada, and from 22% to 33% in Australia.

Month-to-month Shein procuring additionally moved up, reaching 31% within the USA, 29% within the UK, 19% in Canada, and 28% in Australia in 2026. That means these platforms have gotten a part of common buy habits, not simply occasional deal-driven visits.

“These marketplaces are now not occasional low cost choices — they’re turning into embedded in on a regular basis procuring habits,” says Marty Bauer, Ecommerce Knowledgeable at Omnisend. “The most important shift isn’t simply what number of customers have tried them — it’s how usually they’re returning on a month-to-month and weekly foundation.”

Why USA buyers assist tariffs however nonetheless purchase from Chinese language marketplaces in 2026

These market beneficial properties usually are not occurring in isolation. They mirror a broader shift in international cross-border ecommerce, which, in line with Capital One Shopping data, locations the market at $1.21 trillion in 2025. Separate information from the International Post Corporation exhibits how shortly the aggressive panorama has modified: Temu’s share of the newest cross-border orders rose from lower than 1% in 2022 to 24% in 2025, placing it stage with Amazon by that measure.

Within the USA, nonetheless, that progress sits alongside robust assist for home manufacturing and commerce safety. Nearly 46% of American consumers support tariffs on imported goods, while 59% say they are willing to pay more for products labeled “Made in the USA.” On paper, that feels like a transparent vote for home shopping for. In observe, although, Chinese language marketplaces proceed to draw common buyers, suggesting that worth, comfort, and product availability nonetheless outweigh acknowledged preferences in lots of actual buy choices.

That stress is just not particularly shocking to provide chain specialists. As Yao Jin, Affiliate Professor of Provide Chain Administration at Miami College, advised CNBC, “American customers total don’t actually care about an app’s affiliation with any particular nation so long as they’ll discover one thing they need at an reasonably priced worth. (That) is strictly the aggressive benefit of most China-originated apps.” In different phrases, buyers could specific assist for tariffs or home manufacturing in precept, however many nonetheless prioritize low costs and easy accessibility after they truly take a look at.

Even so, the most recent survey suggests buyers who stay energetic on these platforms have gotten extra selective. Amongst customers who diminished or stopped procuring on Chinese language ecommerce platforms, the most typical causes have been worth will increase, product high quality considerations, slower or much less dependable delivery, and extra charges or duties at supply. Within the USA, 23% cited greater costs, 20% pointed to product high quality considerations, and 12% mentioned delivery had turn into slower or much less dependable. One other 12% mentioned further supply charges pushed them away. But it surely’s additionally notable that USA customers most frequently report noticing worth will increase on bigger ecommerce platforms comparable to Amazon and Walmart, displaying that worth stress is just not restricted to Chinese language marketplaces alone.

“Cross-border procuring hasn’t disappeared — however buyers are much less forgiving than they have been a 12 months in the past,” says Bauer. “They’ll chase financial savings, however not if it comes with uncertainty. Tariffs and rising prices have made transparency and predictability a part of the worth equation.”

How can ecommerce manufacturers compete with Chinese language marketplaces in 2026?

There are clear steps ecommerce manufacturers can take to compete in a market the place Chinese language marketplaces are gaining buyers — and tariffs are elevating expectations:

- Compete on predictability, not simply promotions. If buyers are prioritizing sooner delivery and fewer surprises, manufacturers ought to make supply timelines, monitoring, and return insurance policies not possible to overlook.

- Lead with total-cost transparency. With import charges and shock duties contributing to churn — and 25% saying tariff or price reductions would affect their return — readability on full prices is a belief builder.

- Deal with success technique as a messaging technique. The truth that 28% need U.S.-based warehouses or sellers exhibits how a lot success location influences confidence. If in case you have home success, say it clearly.

- Handle high quality considerations head-on. With 20% citing product high quality as the principle motive for pulling again, clear product specs, critiques, and easy return and refund processes turn into levers for conversion.

- Use electronic mail and SMS to cut back uncertainty earlier than it turns into churn. Proactive updates on delivery timelines, coverage modifications, and pricing shifts can stop the “shock issue” that drives abandonment and mistrust.

“When buyers are splitting their budgets throughout extra platforms, retention turns into crucial,” Bauer provides. “Manufacturers that construct direct relationships with clients — as an alternative of relying solely on paid acquisition — shall be in a stronger place long run.”

Methodology

This survey was commissioned by Omnisend and carried out by Cint in June 2024, August 2025, and February 2026. In every wave, 4,000 customers throughout the USA, UK, Canada, and Australia have been surveyed utilizing the identical set of questions to guage how they store on Chinese language marketplaces. Quotas have been utilized for age, gender, and place of residence to create a pattern that represents the whole nation of on-line customers. The margin of error is +/-3%.

As with all survey primarily based on self-reported habits, the findings could also be topic to recall bias. The outcomes are consultant of on-line populations within the surveyed nations and will not absolutely mirror offline or non-English-speaking client teams. Yr-over-year comparisons are primarily based on a constant methodology throughout all three survey waves.

FAQ

What proportion of USA customers store on Temu or Shein in 2026?

In Omnisend’s 2026 survey, 58% of USA customers mentioned that they had shopped on Temu over the previous 12 months, whereas 49% mentioned that they had shopped on Shein. Extra broadly, 71% of USA buyers mentioned that they had used at the very least one Chinese language market, together with Temu, Shein, AliExpress, or TikTok Store, up to now 12 months.

How usually do folks within the UK store on Chinese language ecommerce platforms?

The UK information suggests these platforms have gotten routine procuring locations, not simply occasional cut price stops. In 2026, 32% of UK customers store on Temu month-to-month and 29% on Shein, whereas 75% say they purchased from at the very least one Chinese language market over the previous 12 months.

Are Chinese language market adoption charges rising or reducing in Canada and Australia?

Sure. In Canada, Temu’s adoption rose from 39% in 2024 to 57% in 2026. Shein elevated from 35% to 41%. In Australia, Temu climbed from 52% to 67%, whereas Shein went from 46% to 55%. Australia additionally had the very best total utilization within the research. About 80% of customers shopped on at the very least one Chinese language market up to now 12 months.

How do tariffs on Chinese language items have an effect on costs on Temu and Shein?

Usually, tariffs elevate the landed value of imported items, which makes it more durable for marketplaces constructed on ultra-low costs to maintain these costs unchanged. Reuters reported that Shein and Temu advised USA clients in April 2025 that costs would rise, and that the top of duty-free remedy for a lot of low-value China shipments elevated their prices; Temu additionally shifted towards regionally primarily based sellers and USA-warehouse success to melt the influence.

What are the principle causes customers cease procuring on Chinese language marketplaces?

The most typical causes are greater costs, product high quality considerations, slower or much less dependable delivery, and further charges or duties at supply. Within the USA, for instance, 23% of customers who diminished or stopped procuring cited worth will increase, 20% cited high quality considerations, and 12% pointed to slower delivery or further supply charges.

Source link