{kind=link}

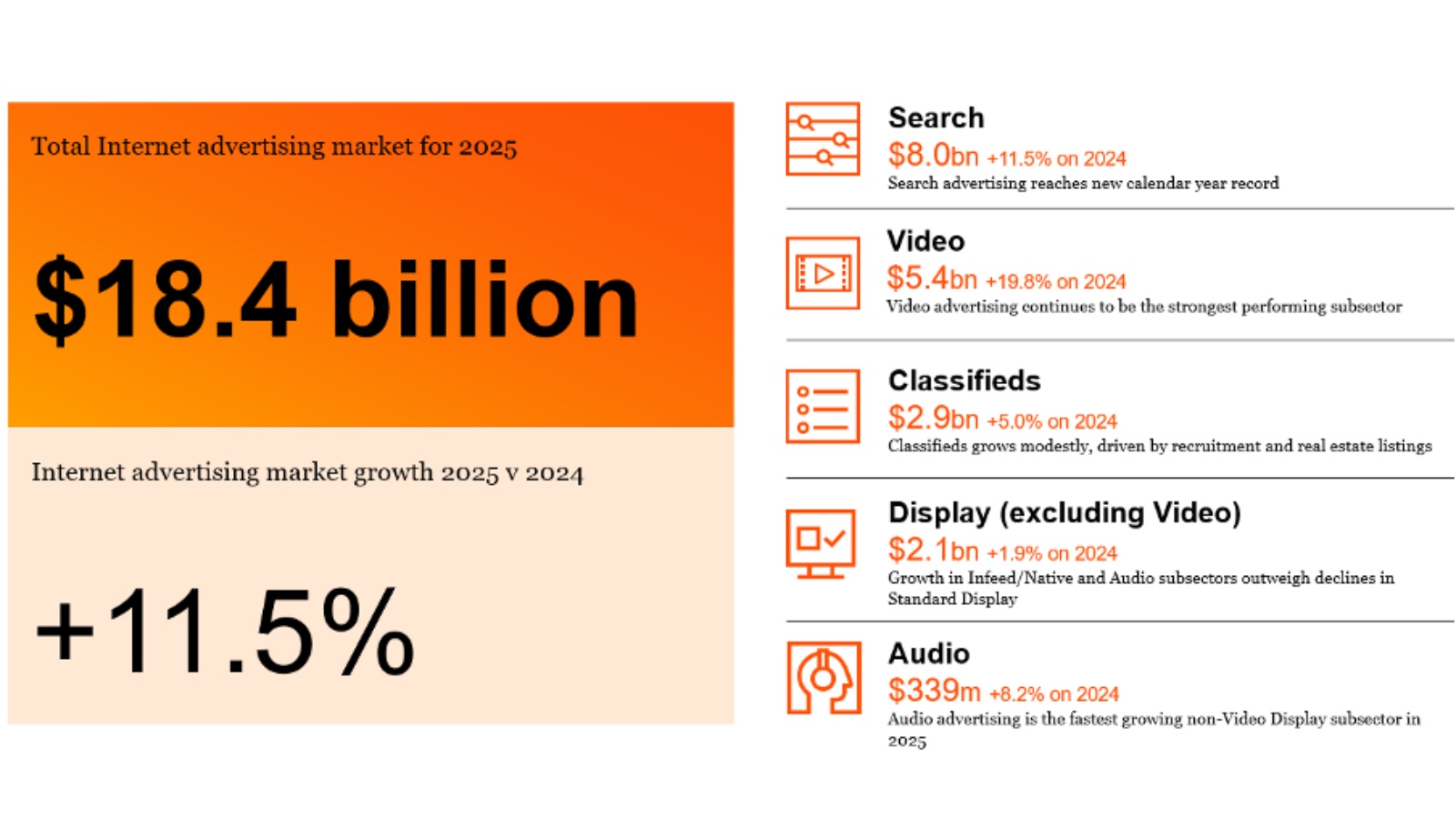

Australia’s web promoting market reached $18.4 billion for the total calendar 12 months 2025, rising 11.5% year-on-year – marking the second consecutive 12 months of double-digit progress, in line with the IAB Australia Internet Advertising Revenue Report (IARR) compiled by PwC Australia and launched on 2 March 2026. The info offers the advertising neighborhood with an in depth image of the place spending flowed, and the place it didn’t.

The headline quantity masks important divergence throughout codecs. Video promoting delivered the standout end result – up 19.8% year-on-year to achieve $5.4 billion – whereas non-video show crept ahead simply 1.9% to $2.1 billion. Search held agency at $8.0 billion, additionally rising 11.5%, recording a brand new annual file. Classifieds expanded 5.0% to $2.9 billion, pushed by recruitment and actual property listings. Audio rounded out the classes at $339 million, up 8.2%, with podcast progress outrunning streaming.

That two-speed market – video and search pulling forward, customary show lagging – is a sample PPC Land has tracked across multiple Australian reporting cycles. The September 2024 quarter already pointed on this course, with video funding propelled by Olympics-related spend. The total-year 2025 end result confirms the trajectory is structural, not seasonal.

The video breakdown: social platforms dominate

Inside video’s $5.4 billion whole, the inner composition shifted sharply throughout 2025. Social video – comprising adverts on Meta platforms, TikTok, Snapchat, Pinterest, LinkedIn, and X – accounted for 40% of whole video funding for the calendar 12 months, reaching $2.2 billion and rising 35.1% year-on-year. Different video (YouTube, SBS On Demand, Foxtel, short-form editorial, and comparable environments) contributed $2.7 billion, up 12.2%. BVOD video – broadcaster video-on-demand throughout 7Plus, 9Now, and 10Play – got here in at $0.5 billion, rising 7.1%, the slowest section inside video.

Social video’s share of whole video elevated by 4 proportion factors in comparison with 2024. That acquire comes at some price to conventional broadcaster environments. For media patrons centered on brand-safe, premium contexts, the info raises questions on the place video budgets are being allotted versus the place audiences are consuming content material.

Related TV continued its longer-term enlargement, with its share of content material publishers’ video stock reaching 57% for the calendar 12 months – up from 51% in 2024 and 50% in 2023. Cell accounted for 30% of that stock, whereas desktop fell to 13%, its lowest share within the reported historic knowledge. The CTV trajectory is per IAB Australia’s video measurement framework published in December 2025, which recognized CTV as probably the most quickly evolving section requiring standardized measurement approaches.

Search: a brand new file, and a constant anchor

Search promoting at $8.0 billion represents 43.8% of whole web promoting expenditure in Australia for 2025 – a share just about unchanged from 43.7% in 2024. The class has held between 43% and 45% of whole spend yearly since 2019, in line with the report knowledge. That stability displays search’s function as a direct-response channel with dependable return on funding calculations; advertisers have maintained dedication whilst brand-building codecs like video attracted incremental finances.

Search additionally exceeded $2 billion for 3 consecutive quarters throughout the 12 months. Within the December 2025 quarter alone, search reached $2,080 million, up 13.4% on December 2024. For the total 12 months, the compound annual progress charge for search since 2019 stands at 11.4%, in line with the report – strong and constant, although beneath video’s 21.8% CAGR over the identical interval.

The December quarter intimately

The report covers each the calendar 12 months and the December 2025 quarter particularly. Whole web promoting expenditure for the December quarter reached $4.9 billion, up 14.4% in comparison with the December 2024 quarter. That acceleration from the full-year charge of 11.5% displays the seasonal weight of retail spending into the fourth quarter.

The report confirms that 52% of whole 2025 web promoting expenditure occurred within the second half of the 12 months, a sample per prior years. In absolute phrases, the second half of 2025 generated $9.5 billion in comparison with $8.8 billion within the first half.

Breaking down the December quarter: video reached $1,510 million (up 15.4%), search hit $2,080 million (up 13.4%), classifieds got here in at $733 million (up 21.2% – the strongest class progress for the quarter), show excluding video was $592 million (up 8.3%), and audio reached $94 million (up 5.1%).

The classifieds end result for the December quarter deserves consideration. A 21.2% year-on-year enhance, pushed by recruitment, actual property, and automotive subsectors, suggests labor market exercise and property transactions remained elevated by way of the top of 2025. PPC Land previously reported on Q3 2024 classifieds patterns exhibiting resilience within the class, and the December 2025 knowledge reinforces that view.

Programmatic and shopping for methodology shifts

For content material publishers’ common show stock, company shopping for through insertion order elevated its share throughout 2025, rising to 46% from 44% in 2024 and 45% in 2023. Direct shopping for fell to fifteen% from 17%, whereas programmatic assured held at 14%. Programmatic RTB/PMP remained at 25%.

The December 2025 quarter confirmed a special image for video particularly. In line with the report, 58% of content material publishers’ video stock was purchased programmatically within the December quarter, regaining share from company (through IO). Wanting on the detailed breakdown for the quarter: for normal show, company through IO dominated at 53%; for infeed/native, programmatic (RTB/PMP) led at 73%; for video, company through IO was 39%, programmatic RTB/PMP at 35%, programmatic assured at 23%, and direct simply 3%.

The seasonal sporting season within the peak Australian broadcast calendar contributed to company IO gaining floor throughout sure 2025 intervals, as high-demand content material environments favour direct-negotiated offers. This shopping for methodology interaction issues for programmatic promoting practitioners, who navigate between automated effectivity and premium stock entry.

Audio: podcasting pulls forward of streaming

The audio market, at $339 million for the total 12 months, sits at 4.5% of whole common show promoting expenditure. Inside that whole, podcast promoting reached $134 million, up 13.5% year-on-year. Streaming audio got here in at $205 million, rising 5.0%. Podcasting’s sooner progress charge – greater than double that of streaming audio – is per the viewers shift in direction of long-form on-demand audio content material.

For the December quarter, whole audio reached $94.2 million, approaching the $100 million quarterly threshold. Podcast spend for the quarter was $35.8 million (up 6.5% on December 2024), streaming $58.4 million (up 4.3%). Each subsectors grew in opposition to the prior 12 months comparative quarter.

The audio end result sits inside a broader IAB Australia give attention to digital audio measurement and requirements. IAB Australia released alcohol advertising compliance guides for digital audio in August 2025, reflecting the class’s progress as an promoting medium requiring its personal regulatory frameworks.

Trade class shifts: finance up, automotive down

The report’s trade class knowledge covers reported common show promoting from content material publishers – notably excluding Meta, Google, X, Snapchat, Spotify, TikTok, Pinterest, Amazon, LinkedIn, and Foxtel common show promoting. With that scope in thoughts, the highest 5 classes for the total calendar 12 months 2025 have been retail (17.5% share), automotive (13.3%), leisure & media (10.0%), finance (8.7%), and FMCG (6.3%).

Retail maintained its place because the main class for the fifth consecutive 12 months. However the directional actions are instructive. Finance elevated its share from 8.0% in 2024 to eight.7% in 2025 – a acquire of 0.7 proportion factors. Insurance coverage added 1.2 proportion factors to achieve 4.3%. Automotive, against this, fell 1.5 proportion factors from 14.8% to 13.3%, and leisure & media dropped 1.4 proportion factors from 11.4% to 10.0%.

For the December 2025 quarter particularly, retail strengthened additional to 19.8% of reported common show – up from 17.3% in December 2024. Telecommunications recorded the biggest acquire for the quarter, including 1.8 proportion factors. Know-how fell 2.2 proportion factors to 2.5%.

video promoting preferences, FMCG and dwelling merchandise classes confirmed the strongest over-indexing in direction of video relative to their common show share. FMCG’s share of 2025 video spend (8.6%) exceeded its common show share (6.3%) by 2.3 proportion factors. House merchandise equally over-indexed by 1.6 proportion factors. Actual property, conversely, under-indexed video by 3.4 proportion factors, reflecting the format’s lesser relevance for property search contexts.

Social show and video: approaching one-fifth of whole market

Social show and video mixed – encompassing all show codecs on Meta platforms, TikTok, Snapchat, Pinterest, LinkedIn, and X – reached 17.6% of whole web promoting expenditure for calendar 12 months 2025, up from 16.0% in 2024. In absolute phrases, this represents $3.2 billion. Non-social show and video, at 21.2%, declined from 21.8%.

For the December 2025 quarter, social show and video accelerated to 19.5% of the whole market ($957 million for the quarter), up from 17.8% in December 2024. The trajectory suggests social platforms are heading in the right direction to strategy parity with non-social show and video inside a couple of quarters if present progress charges persist.

Gai Le Roy: progress is selective

Gai Le Roy, CEO of IAB Australia, commented on the full-year outcomes: “The 2025 outcomes present a market that’s rising, however selectively. Total funding elevated strongly, pushed primarily by video and search, whereas different show environments noticed extra modest motion. Social video and podcasting proceed to outperform the market.”

Le Roy additionally highlighted the altering advertiser base: “Whereas the massive media companies stay vital drivers of scale, we’re additionally seeing robust funding from unbiased companies, high-growth manufacturers managing their very own media, and SMEs. Established advertisers proceed to increase in-house functionality, and we’re seeing elevated funding from Chinese language and different worldwide manufacturers searching for to attach with Australian audiences.”

That shift in advertiser composition has structural implications. If the expansion in direct-to-market manufacturers and worldwide entrants continues, it may reshape the stability between company insertion orders and programmatic shopping for channels over coming years.

Lengthy-term context: from $9.3bn to $18.4bn in six years

The historic knowledge within the report offers perspective on the tempo of market enlargement. Australia’s web promoting market stood at $9.3 billion in 2019. It contracted 3.7% within the pandemic 12 months of 2020 to $9.6 billion, earlier than recovering sharply to $13.0 billion in 2021 (a 36% leap). Progress moderated to 9.1% in 2022 ($14.2 billion) and slowed additional to three.7% in 2023 ($14.7 billion), earlier than accelerating once more to 12.2% in 2024 ($16.5 billion) and 11.5% in 2025 ($18.4 billion).

Video’s compound annual progress charge since 2019 stands at 21.8%, in comparison with 11.4% for search, 9.5% for classifieds, and simply 2.3% for show (excluding video). The divergence confirms a long-running structural shift in promoting format preferences, not merely a short-term pattern. PPC Land reported on the FY25 mid-year figures in September 2025, when the 12-month whole reached $17.2 billion – the December half-year knowledge now provides roughly $1.2 billion to that working whole.

Methodology observe

The IARR is compiled by PwC Australia on behalf of IAB Australia, drawing on expenditure knowledge submitted immediately by collaborating corporations. Knowledge seize for the IARR commenced within the March 2002 quarter. Figures are based mostly on gross commissionable promoting income – the quantities charged to the advertiser earlier than company rebates. The report doesn’t represent an audit underneath Australian Auditing Requirements. For platforms together with Meta, Google, TikTok, Amazon, Spotify, LinkedIn, Pinterest, Snapchat, X, and Foxtel, which don’t disclose revenues by geography or product line, estimates are developed by way of earnings evaluation, analysis agency knowledge, and interviews with company and writer executives.

Contributors to the report’s verified knowledge embody Acast, ARN Media, carsales.com, Each day Mail Australia, Area, The Guardian, MamaMia, Information Corp Australia, 9, Paramount, REA Group, SBS, Search, Seven West Media, Triton Digital, and Yahoo.

Timeline

Abstract

Who: IAB Australia, in collaboration with PwC Australia, compiled and launched the info. The report’s findings have been commented on by Gai Le Roy, CEO of IAB Australia. Knowledge contributors embody main Australian media corporations and digital publishers; platforms together with Meta, Google, TikTok and others have been included through PwC estimates.

What: The IAB Australia Web Promoting Income Report for calendar 12 months 2025 and the December 2025 quarter reveals the Australian web promoting market reached $18.4 billion for the total 12 months 2025, rising 11.5% year-on-year. Video grew 19.8% to $5.4 billion; search grew 11.5% to $8.0 billion; classifieds grew 5.0% to $2.9 billion; show excluding video grew 1.9% to $2.1 billion; audio grew 8.2% to $339 million. The December 2025 quarter alone reached $4.9 billion, up 14.4%.

When: The report covers the calendar 12 months ended 31 December 2025 and the quarter ended 31 December 2025. It was launched on 2 March 2026 by IAB Australia.

The place: The report covers the Australian web promoting market. The report was ready by PwC Australia and printed by IAB Australia, the height commerce affiliation for internet advertising in Australia.

Why: The IARR is an ongoing trade measurement initiative designed to offer an correct barometer of web promoting expenditure progress in Australia. For the advertising neighborhood, the info issues as a result of it confirms the shift of promoting budgets towards video – notably social video and related TV – whereas highlighting that non-video show codecs are rising extra slowly than the broader market. The finance and insurance coverage classes are gaining show share; automotive and leisure are dropping it. Company insertion-order shopping for is reclaiming share from direct shopping for, whereas programmatic stays dominant in video. These indicators have an effect on finances allocation, platform technique, and measurement priorities for advertisers and companies working within the Australian market.